.png?width=651&height=365&name=68005%20-%20GK3%20Blog%20-%20Learning%20Center%20325x155@2x%20(1).png)

I watched a fund manager celebrate after a call with an RIA last month. The conversation went well. The advisor asked smart questions. They talked about fit, portfolio construction, and next steps.

Three weeks later, the advisor stopped responding.

This happens more than fund managers realize. You get the meeting. The advisor shows genuine interest. Then nothing. No allocation. No follow-up. Just silence.

The problem isn't your pitch. It's what happens after you hang up.

The Invisible Graveyard Where Deals Die

Here's what actually happens after that positive call.

The advisor returns to their desk with enthusiasm about your fund. They've got questions answered. They understand the strategy. They're ready to move forward.

Then they hit the wall.

They need to present your fund to their investment committee. That committee will ask questions the advisor can't answer off the top of their head. Questions about fee structures in different scenarios. Questions about how the fund performs in downside markets. Questions about operational due diligence.

The advisor doesn't have those answers documented. They'd need to pull together a presentation from scratch. They'd need to compile information from your fact sheet, your prospectus, and their notes from the call.

That's hours of work.

So they put it off. They get busy with other priorities. Your fund moves from "excited about this" to "I'll get to it later" to "what was that fund again?"

But here's the gap: even advisors who've done their homework still don't have what they need to get internal approval.

What Investment Committees Actually Require

Investment committees at RIA firms aren't rubber stamps. They're gatekeepers with formal approval processes.

David Canter, head of the RIA segment at Fidelity Custody & Clearing Solutions, puts it clearly: "Decisions tend to get reviewed more thoroughly by committees than they would be by an advisor working alone." These committees exist specifically to provide oversight over investment processes.

That means even when an advisor personally loves your fund, they face a rigorous internal vetting process.

The committee will ask about:

- Fee structures across different investment scenarios

- Liquidity terms and redemption processes

- Strategy differentiation from competitors

- Team background and operational integrity

- Platform availability on their custodian

- Performance in downside scenarios

Your fact sheet doesn't answer these questions. Your prospectus is too dense. Your sales deck was built for a conversation, not for documentation.

The advisor needs something else entirely.

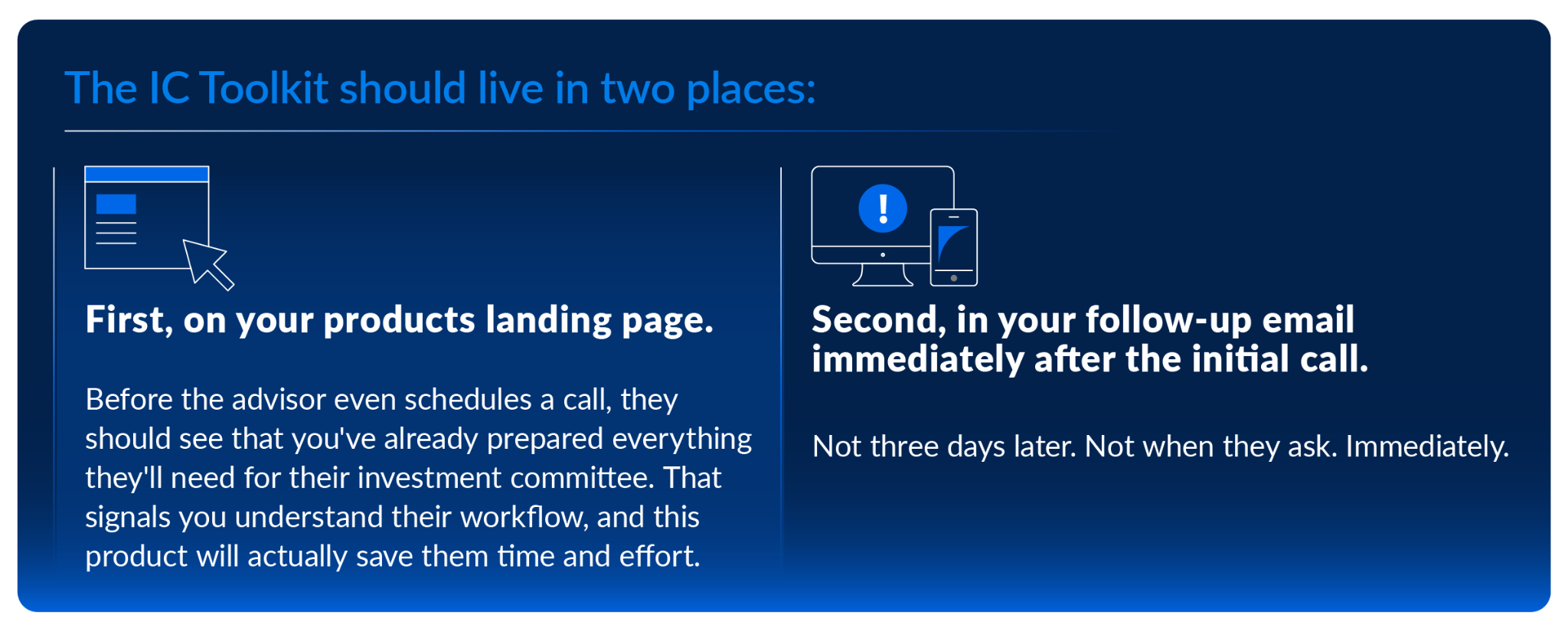

What an IC Toolkit Actually Looks Like

At GK3, we've built something called an Investment Committee Toolkit for our clients. It's not a sales tool. It's an internal advocacy toolkit.

What goes into a toolkit varies by fund, asset class, and the specific gaps in their current materials. For one recent client, we built a four-document toolkit that included an Investment Committee FAQ, a Platform Availability document, a Client-Facing Explainer, and a Portfolio Fit Guide showing exactly where the fund fits in different client allocation scenarios.

Let me walk you through four core documents that frequently show up in these toolkits, though your fund may need different or additional materials depending on where advisors are getting stuck.

The IC FAQ

This addresses the anxiety: "I don't have the answers to all of the questions my committee will ask."

The IC FAQ is a one-page document that anticipates and answers the most common investment committee questions. Not generic questions. The specific ones that come up for your asset class.

For a real estate private credit client, that meant questions about loan-to-value ratios, subordination structures, and geographic concentration risk. For a value-add multifamily manager, it meant questions about renovation timelines, exit strategies, and interest rate sensitivity.

The document uses plain language. It provides specific answers. It saves the advisor from having to compile this information themselves.

The Platform Availability Document

This addresses the anxiety: "I don't know if my clients can even access this."

Platform availability is often the first practical question after interest is established. Advisors need to know if your fund is available on Fidelity, Schwab, Pershing, or whatever custodian they use.

If the RIA isn’t sure what platform your fund is on, the conversation ends.

This should be a simple one-page document that clearly shows where advisors can access your fund. No hunting through your website. No calling your sales team. Just a clear, visual confirmation.

The Client-Facing Explainer

This addresses the anxiety: "I don't have time to create a presentation and translate this into plain language my clients will understand."

Your advisor needs to hand something downstream to their clients. They can't just forward your prospectus. They need a document that explains your fund in language their clients will understand.

This is where most fund marketing falls apart. You speak in sponsor-speak. Your advisor needs client-speak.

The client-facing explainer translates your strategy, your risk profile, and your value proposition into language that works in a client meeting. It removes both the translation and time burden from the advisor.

When You Should Actually Deploy These Materials

Here's where most fund managers get the timing wrong.

They wait until the advisor asks for information. They respond reactively. They send materials only when specifically requested.

That's too late.

The email should be direct:

"Thanks for the call today. I know the next step is presenting this to your investment committee. I've attached the materials we've prepared specifically for that process: an FAQ addressing common committee questions, confirmation of platform availability, a client-facing explainer you can use downstream, and [other relevant documents]. These should save you the work of compiling this yourself."

You're not being pushy. You're removing friction.

Why This Isn't Standard Practice Yet

Most fund managers stick to the industry playbook: prospectus, fact sheet, maybe a sales brochure.

They think they've checked the boxes. They assume that's enough.

It's not.

Those documents serve a purpose, but they don't serve the purpose advisors actually need. They don't help advisors navigate their internal approval processes. They don't save advisors time. They don't address the specific anxieties that cause deals to stall.

The gap exists because fund managers think about content from their own perspective, not from the advisor's operational reality.

Here's the shift: buyers are 80% through their decision-making process before they contact you.

By the time an advisor reaches out, they've already done significant research. They've already built conviction. What they lack isn't interest. It's the operational tools to move that interest through their firm's approval process.

The Operational Advantage Nobody Talks About

Fund managers obsess over performance. They optimize their pitch decks. They refine their differentiation story.

Those things matter. But they're not where deals get lost.

When you provide advisors with ready-made IC materials, you create a competitive advantage that has nothing to do with your fund's returns. You reduce friction. You save time. You demonstrate that you understand how advisors actually work.

When you provide advisors with ready-made IC materials, you create a competitive advantage that has nothing to do with your fund's returns. You reduce friction. You save time. You demonstrate that you understand how advisors actually work.

According to recent B2B research, the typical buying team now includes nearly 12 individuals. More than double the average from 2020. That's not just true in tech sales. It's increasingly true in RIA firms with formal investment committees.

Your advisor isn't just presenting to one committee chair. They're navigating consensus across multiple stakeholders with different concerns and information needs.

The more complex that internal process becomes, the more valuable your IC Toolkit becomes.

What Success Actually Looks Like

Most fund managers measure success by meetings booked. That's the wrong metric.

The right metric is internal approvals secured.

When you shift your thinking from "how many meetings did we get" to "how many advisors successfully presented our fund to their investment committee," everything changes.

You stop optimizing for the meeting itself. You start optimizing for what happens after the meeting.

You stop thinking about your content as sales collateral. You start thinking about it as operational support.

You stop measuring activity. You start measuring outcomes.

The fund that wins isn't the one with the best pitch. It's the one that made the advisor's internal job easiest.

The Real Question Fund Managers Should Ask

After your next positive call with an advisor, ask yourself this:

What does this advisor need to take our fund to their investment committee, and have I given it to them before they have to ask?

If the answer is no, you're leaving deals on the table.

The meeting isn't the finish line. It's the starting gun for an internal approval process you have no visibility into.

Your job isn't to win the meeting. Your job is to give the advisor everything they need to win internally.

That's a different game entirely.

At GK3 Capital, we help fund managers build IC Toolkits that actually move advisors through their internal approval processes. We've seen what happens when you shift from sales-focused content to operations-focused content.

The deals that used to stall start closing.

If you're tired of watching positive meetings turn into radio silence, let's talk about what your advisors actually need to say yes internally.

{kind=link}